Why this amendment is about fixing the revenue record gap — not changing land use law

Headway Partners | Real Estate & Regulatory Advisory

Most commentary on the U.P. Revenue Code (Amendment) Ordinance, 2026 starts from the wrong assumption. It treats the amendment as if it were meant to simplify approvals by removing a separate Section 80 hurdle that developers had to clear before building. That is not what was happening on the ground, and it is not what this Ordinance really changes.

The real issue was downstream. Development Authorities were already sanctioning plans on Gata-identified land. The friction arose later, when revenue records continued to show that same land as agricultural and lenders, buyers, and revenue officials were forced to work around the mismatch. That is the gap this Ordinance closes. It does not hand Development Authorities a new power to change land use, and it does not rewrite the planning law framework in Uttar Pradesh.

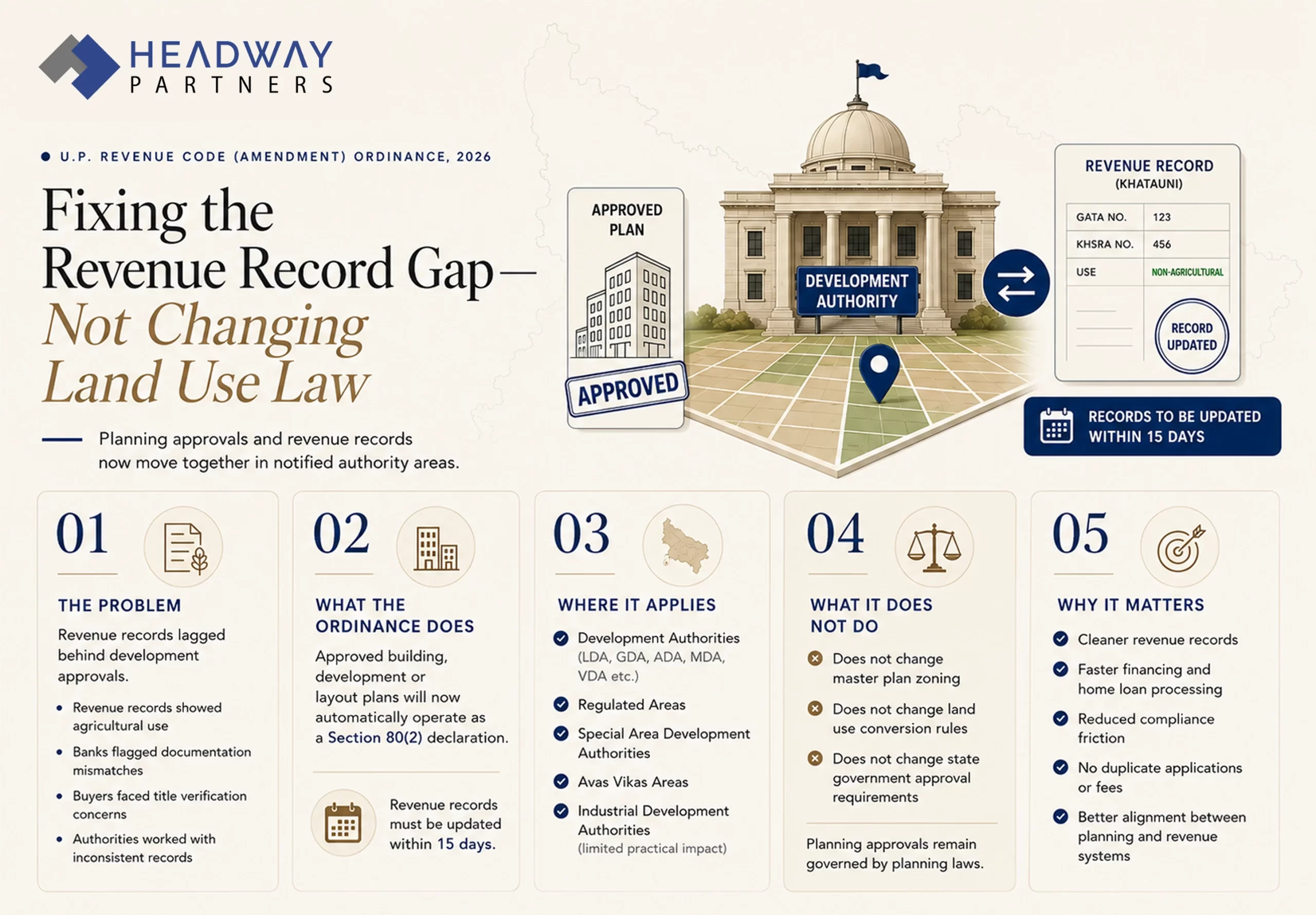

Key takeaways: In notified Development Authorities, Regulated Areas, Special Area Development Authorities and Avas Vikas areas, an approved building permission, development permission or layout plan will now operate as a Section 80(2) declaration; the revenue records are to be updated within fifteen days; no fee is payable for that declaration; the amendment does not authorise any change in land use without the approvals required under planning law; and for land outside these notified areas, the older Section 80 process continues.

What the amendment says

The amendment inserts two new provisos into Section 80(8) of the U.P. Revenue Code, 2006.

Section 80 of the Revenue Code deals with what practitioners call a “non-agricultural use declaration” — a formal entry in the revenue records acknowledging that a piece of agricultural Gata/Khasra land is being used, or is proposed to be used, for non-agricultural purposes such as residential, commercial, or industrial development. Under Section 80(1), if the land is already being so used, the Sub-Divisional Officer can record a declaration. Under Section 80(2), if the use is proposed, the bhumidhar can apply for one.

The new provisos say: if your land lies within the notified area of a Development Authority (LDA, GDA, ADA, MDA, VDA, and others constituted under the U.P. Urban Planning and Development Act, 1973), a Special Area Development Authority, a Regulated Area, or the U.P. Housing and Development Board (Avas Vikas Parishad), Industrial Development Authorities — and the competent Authority has granted a building permission, development permission, or layout plan approval — then that approval will itself be treated as a declaration under Section 80(2). The revenue records must be updated within fifteen days. And no fee shall be charged for the declaration.

The real bottleneck was in the records, not the approval process

This is the point on which much of the public commentary has been imprecise.

The common narrative has been that developers were trapped in a “double window” — first obtaining Development Authority approval, then separately approaching the SDO for a Section 80 declaration, paying a fee, waiting for an inquiry, and only then moving ahead with confidence. That description suggests the Section 80 process was functioning as a mandatory approval-stage hurdle.

The documents show a different reality.

Sanction letters issued by six Development Authorities across Uttar Pradesh — GDA (Ghaziabad), LDA (Lucknow), MDA (Meerut), VDA (Varanasi), ADA (Agra), and ADA (Ayodhya) — all publicly available on the UP RERA portal as part of registered project documentation, show the same pattern. They identify the land by Gata/Arazi/Khasra numbers and grant approval for construction on that land. None of them makes a prior or concurrent Section 80 declaration from the SDO a condition of approval and the Development Authorities in UP have been approving building plans and layout plans on Gata-identified agricultural revenue land without making Section 80 a precondition. That has been the consistent practice across jurisdictions and use types.

So what was the actual problem?

The problem was downstream, in the revenue records and at the lending counter — not at the Authority approval stage.

Once a developer received a DA approval and commenced construction, the Khasra/Khatauni records in the revenue register continued to show the land as agricultural. The planning authority had sanctioned development. Construction was underway. But the revenue records had not caught up. This created a legal gap that had two practical consequences:

First, banks and lenders — whose legal teams are rightly careful about the title chain — flagged this mismatch when evaluating project finance or home loan applications. A Khasra number that still reads “agricultural” in the Khatauni, even though a Development Authority has sanctioned construction on it, creates a documentation gap. Many lenders conditioned disbursements on the borrower producing a Section 80 declaration — not because the law required it before construction, but because it gave their legal team a clean revenue record to rely on.

Second, there was a latent legal risk — less exercised in practice, but real in law. Section 80(1) of the Revenue Code empowers the SDO to initiate proceedings suo motu when he finds that land is already being used for non-agricultural purposes. Rule 86 of the U.P. Revenue Code Rules, 2016, expressly prescribes the procedure for such suo motu action: the SDO issues notice to the bhumidhar, holds an inquiry, and makes a declaration. The Allahabad High Court has confirmed this power in Ishan Chaudhary and Another v. Union of India and Others (Writ C 10619 of 2025, decided 10 April 2025) and in Sri Kanhaiya Lal Trust and Another v. State of U.P. and Others (Writ C 3955 of 2022, decided 17 April 2023). The Lekhpal’s periodic Girdawari inspections are the mechanism through which the revenue machinery would detect construction on Gata land — and the Lekhpal is bound by law to report such use to the Naib Tahsildar, who in turn would escalate to the SDO.

In practice, this suo motu power was dormant in Development Authority areas. The administrative bandwidth was not there to pursue it systematically across thousands of Khasra parcels undergoing development. No reported High Court judgment has been found where an SDO actually initiated Section 80(1) proceedings against a developer in a DA jurisdiction. But the latent exposure existed in law, and experienced practitioners were aware of it.

The 2026 Ordinance addresses all of this — the revenue record gap, the banking documentation demand, and the latent suo motu risk — in one stroke. By deeming the Development Authority’s approval itself as a Section 80(2) declaration, and mandating a fifteen-day revenue record entry, the Ordinance ensures that the Khatauni is updated automatically and promptly whenever a lawful planning approval is granted. There is no separate application, no fee, no inquiry, and no scope for revenue authorities to sit on the entry.

Where the amendment applies — and where it does not

The deeming fiction in Section 80(8) applies specifically to land within the notified areas of Development Authorities constituted under the U.P. Urban Planning and Development Act, 1973 — authorities like LDA (Lucknow), GDA (Ghaziabad), ADA (Agra and Ayodhya), MDA (Meerut), VDA (Varanasi), and their equivalents. It also applies to Regulated Areas notified under that Act, Special Area Development Authorities, and Avas Vikas Parishad project areas.

One important clarification: although this Ordinance is applicable to Industrial Development Authorities — NOIDA, Greater Noida, YEIDA, and similar bodies constituted under the U.P. Industrial Area Development Act, 1976, however in practicality this amendment does not seem of any significant changes. The reason is that these authorities operate on a fundamentally different model. They acquire land compulsorily, the land vests in the Authority, and after master planning, zonal planning and infrastructural development by these authorities, plots are allotted to individuals and developers on a leasehold basis — typically on 90-year leases. There is, in practical terms, no privately-held freehold Gata land within NOIDA, GNIDA, or YEIDA’s developed sectors on which an independent building or layout approval would be granted by the Authority to a private freehold landowner. The deeming fiction has no surface area to operate on in these jurisdictions, and they fall outside the Ordinance’s scope entirely.

For land outside any Development Authority or Avas Vikas notified area — which is a large portion of agricultural land in UP, spanning rural tehsils, districts without an active Development Authority, and peri-urban pockets beyond Master Plan boundaries — the 2026 Ordinance changes nothing. The pre-existing Section 80 regime continues in full.

In such areas, a landholder who wants a non-agricultural use declaration must still file an application before the SDO under Section 80(1) or 80(2), go through the prescribed inquiry under the Revenue Code Rules, 2016, and wait for the standard timeline — which can vary significantly from tehsil to tehsil. There is no fifteen-day mandatory deadline here. There is no deemed declaration. And the suo motu risk from the SDO, while equally applicable in law, is similarly dormant in practice.

There is one question worth tracking for landowners outside Authority areas: the second new proviso inserted by the Ordinance — which says no fee shall be charged for a declaration under Section 80(2) — is textually broad. It does not explicitly restrict itself to cases arising from the deeming fiction in Authority areas. Read literally, it could support an argument that the fee waiver applies to all Section 80(2) declarations statewide. This has not been officially clarified. Until the Rules are amended or a Government circular is issued, practice at the Tehsil level is likely to vary. It is worth watching, and worth raising in pending or upcoming Section 80(2) applications outside Authority areas.

What this does not do: it does not change land use by itself

We should address this directly because it has been creating confusion.

The 2026 Ordinance does not — in any way — authorise Development Authorities to change land use categories (industrial to residential, residential to commercial, and so on) without State Government approval. These are entirely different legal regimes.

The master plan — which designates zones as industrial, residential, commercial, or public/semi-public — is governed by the U.P. Urban Planning and Development Act, 1973, not the Revenue Code. Any significant change to land use extents in the master plan requires State Government approval under Section 13 of the 1973 Act. A Development Authority’s board cannot resolve to rezone a sector through an internal decision and start sanctioning maps accordingly. That framework is completely untouched by the Revenue Code amendment.

And as a point of basic legal literacy worth repeating: even the Section 80(2) declaration itself — whether arising from the new deeming fiction or from a direct application — does not amount to a change of land use. The Revenue Code says this explicitly, and the 2019 Amendment Act reinforced it. The land continues to be treated as agricultural in revenue classification. What changes is that the revenue records carry an entry reflecting the declared or proposed non-agricultural use — which matters considerably for financing, due diligence, and title purposes, but it is not a planning decision.

What this means in practice

For developers and landowners working within GDA, LDA, ADA, MDA, VDA, or similar Development Authority notified areas, the correct approach after this Ordinance is: obtain your building or layout approval from the Authority, and then follow up actively with the relevant SDO or Tahsildar to ensure the fifteen-day revenue record entry is actually made. Do not assume it will happen automatically. The U.P. Revenue Code Rules, 2016 are yet to be formally amended to prescribe the exact inquiry procedure for deemed declarations, and ground-level implementation will take time to stabilize. But the statutory entitlement is now clear. If revenue officers ask for a separate Section 80 application or a fee in DA areas where you have a valid planning approval, the Ordinance gives you a clear answer.

For individual buyers in approved plotted colonies within notified master plan areas, this should translate into cleaner revenue record entries and faster home loan processing — provided the fifteen-day obligation is enforced. Banks and lenders who have been conditioning project finance or home loan disbursements on Section 80 declarations can now, in DA jurisdictions, rely on the sanctioned building or development plan and the consequent revenue entry instead.

For land outside Development Authority or Master Plan areas, the pre-existing process applies without change. The Section 80 application before the SDO, the prescribed inquiry, and the standard timelines all continue. Developers working in such areas should also factor in the broader compliance requirements that apply — land conversion or diversion permissions under applicable State policies, zonal or district plan compliance where relevant, environmental clearances where triggered, and local body NOCs. The Section 80 declaration is one step in what is often a longer chain for such land.

Why this matters

There is a broader observation worth making. The 2026 Ordinance is not a dramatic overhaul of UP’s land use or planning framework. It is a precise, targeted fix to a specific problem: the misalignment between planning records (where the Development Authority’s files reflect an approved project) and revenue records (where the Khatauni still shows agricultural land). That misalignment has been a source of friction for developers, a documentation headache for lenders, and a latent legal anomaly sitting in revenue records across Development Authority areas.

What the Ordinance does is align the two records automatically, promptly, and without cost, whenever a valid planning approval exists. It does not change who decides land use, does not expand the powers of Development Authorities over master plan amendments, and does not convert agricultural land into non-agricultural land in any legal sense. It simply ensures that when the planning system moves, the revenue record moves with it — within fifteen days, by statutory mandate.

That makes this a meaningful reform. But its value lies in understanding it precisely. Read correctly, it reduces friction in records, financing, and compliance. Read loosely, it can easily be mistaken for a broader land use reform that it is not.

Headway Partners advises on real estate transactions, land acquisition, urban planning regulations, and development compliance across the NCR, Uttar Pradesh, and Haryana. If you are structuring a land acquisition, seeking project finance, evaluating title risk, or planning a development in Uttar Pradesh, this amendment has direct implications for your documentation, timelines, and execution strategy. We advise developers, landowners, investors, and lenders on how to apply these changes in live transactions and projects.